Liquidity risk & ALM analytics without blindspots

Monitor, stress test, and explain intraday and structural liquidity across entities and desks - covering cash flow management, regulatory (EBA LCR, NSFR, PRA110, FED FR2052a...) and internal liquidity metrics on a single, transparent platform.

Get a demo

Why global and regional banks choose Opensee for liquidity risk analytics

Key capabilities of Opensee for liquidity risk analytics

Single liquidity data hub across entities & desks

Ingest and centralize contractual and behavioral cash flows, positions, funding instruments, and reference data across banking and trading books. Aggregate and analyze liquidity exposures by legal entity, branch, business line, desk, product, or currency, with full drill-down to individual transactions and cash flow projections.

Ingestion of contractual and behavioral cash flows for all relevant products

Coverage of loans, deposits, securities, repos, derivatives, and off-balance sheet items

Consistent views across treasury, risk, finance, and regulatory reporting

Multi-entity, multi-currency, multi-book aggregation with versioning and audit trails

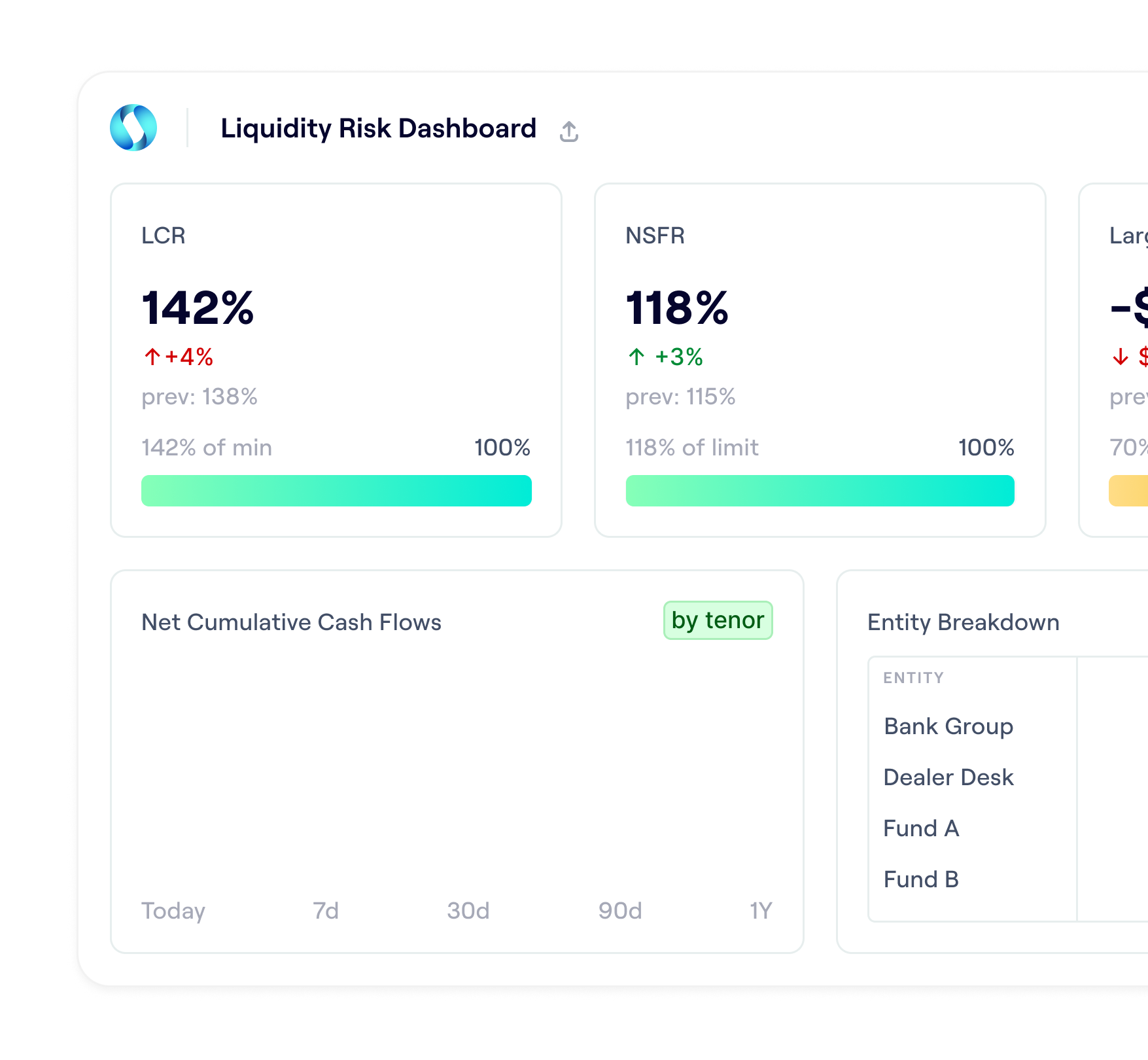

Transparent regulatory and internal liquidity calculations

Calculate, monitor, and explain key regulatory liquidity metrics such as LCR, NSFR, and PRA110, alongside internal liquidity indicators used for ALM and risk management. Opensee provides full transparency from reported ratios down to underlying cash flows and assumptions.

Native LCR and NSFR calculations with configurable run-off factors and haircuts

PRA110 and jurisdiction-specific adaptation with evolving data model

Internal liquidity metrics (cumulative gaps, survival horizons, concentration measures, HQLA composition)

Drill-down from ratios and KPIs to positions, instruments, and projected flows

Liquidity stress testing across time horizons

Define and run regulatory and internal liquidity stress scenarios—market-wide shocks, funding stresses, name-specific events, or intraday cash disruptions—and assess their impact on cash flow gaps, liquidity buffers, and regulatory ratios across entities and currencies.

Apply regulatory and internal stress scenarios

Customize scenarios by entity, business line, currency, or product

Visualize impacts on gaps, buffers, and liquidity ratios

Scenario comparison with drill-down to affected instruments and cash flows

AI-driven liquidity data quality and controls

Combine rule-based controls and statistical analysis to identify data quality issues and abnormal movements in liquidity metrics. Visual indicators and alerts allow treasury and risk teams to investigate anomalies and validate data before it is used for regulatory reporting, internal governance, or management decisions.

Automated completeness, consistency, and business checks on incoming data

Statistical outlier detection in cash flows, balances, and liquidity metrics

Workflows for investigation, adjustment, and sign-off

Visual alerts for significant changes in LCR, NSFR, gaps, and internal indicators

Explore more Opensee solutions

Counterparty Credit Risk

SA-CCR, IMM-CCR, SA-CVA, and xVA calculations with full explainability—at any granularity, with sub-second response times on billions of exposures.

Market Risk

Monitor, explore, and explain real-time VaR, sensitivities, and stress scenarios. Be ready for FRTB SA and IMA, with zero trade-offs between regulatory accuracy and 1LOD/2LOD explainability.

Banking Credit Risk

Monitor credit risk across retail, SME, and corporate portfolios by exploiting PD, LGD, and EAD outputs, analyzing provisions and RWA, and identifying emerging risks early.

Collateral & Margin Management

Monitor SIMM exposure, optimize collateral allocation, and automate margin workflows in real time, with AI-driven insights and full regulatory audit trails.