IRRBB analytics without blind spots

Monitor, stress test, and explain interest rate risk in the banking book across entities and desks - covering EVE, NII, repricing gaps, and internal ALM metrics on a single, transparent platform aligned with supervisory expectations.

Get a demo

Why banks choose Opensee for IRRBB analytics

Key capabilities of Opensee for IRRBB analytics

Single IRRBB data hub across entities and desks

Ingest and centralize balance sheet positions, cash flow schedules, repricing dates, behavioral assumptions, and reference data across the banking book. Aggregate and analyze interest rate risk exposures by legal entity, branch, business line, product, or currency, with full drill-down to individual instruments and cash flow profiles.

Ingest cash flows and repricing data

Coverage of loans, deposits, securities, non-maturing deposits, and optionality

Consistent views across ALM, risk, finance, and regulatory reporting

Multi-entity, multi-currency aggregation with versioning and audit trails

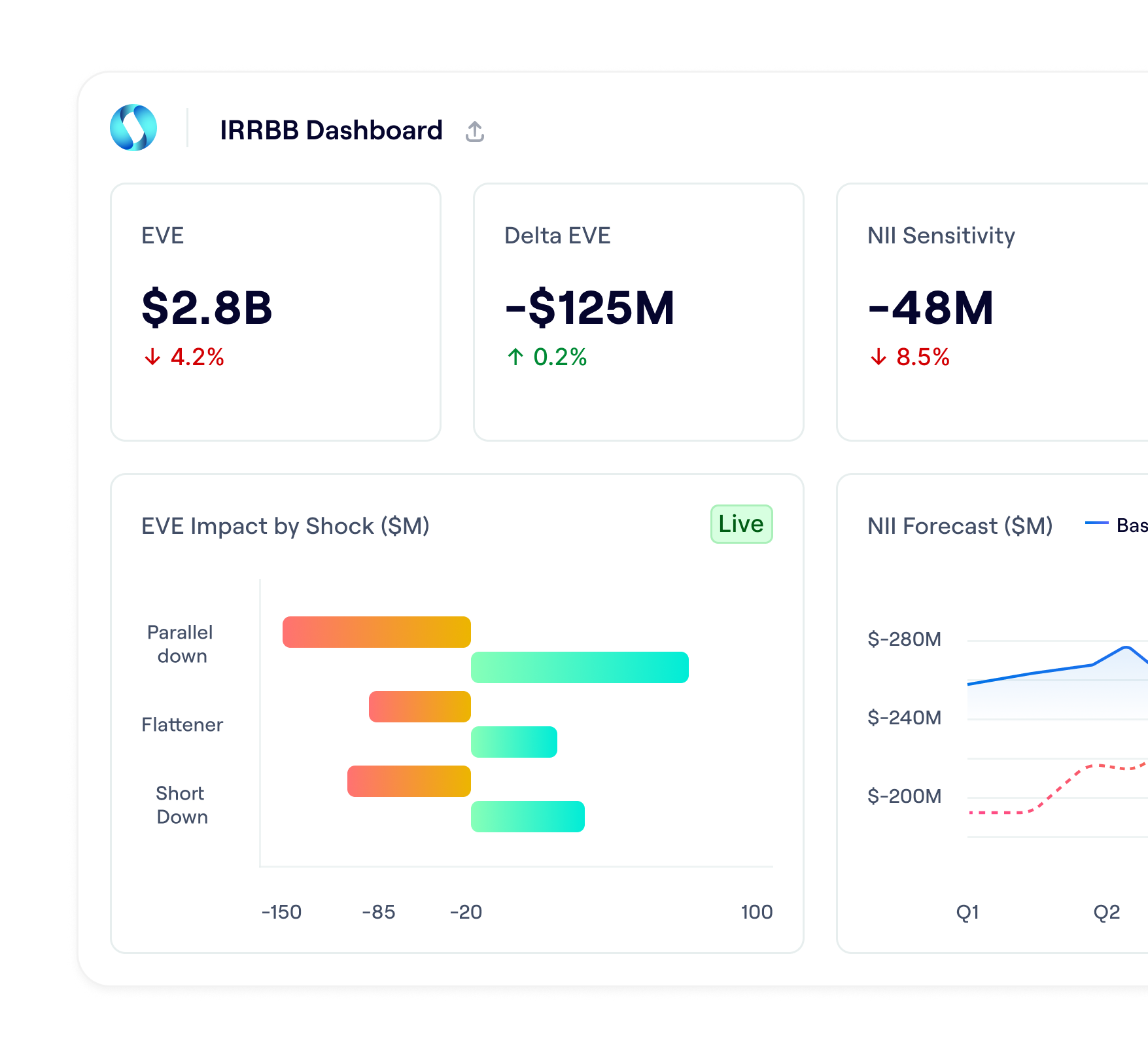

Transparent IRRBB metrics and sensitivity analysis

Calculate, monitor, and explain key IRRBB indicators such as EVE and NII sensitivities, alongside internal ALM metrics used for balance sheet management. Opensee provides full transparency from reported metrics down to underlying cash flows, repricing buckets, and behavioral assumptions.

EVE and NII sensitivity analysis under supervisory and internal scenarios

Support for parallel and non-parallel yield curve shocks

Internal ALM indicators (repricing gaps, duration metrics, margin sensitivity)

Drill-down from IRRBB metrics to instruments, cash flows, and assumptions

Interest rate stress testing across time horizons

Define and run supervisory and internal IRRBB scenarios—including yield curve shocks, basis risk, and changes in behavioral assumptions—and assess their impact on EVE, NII, and repricing gaps across entities and currencies.

Application of supervisory IRRBB shock scenarios

Custom scenarios by entity, product, currency, or assumption set

Clear visualization of impacts on EVE, NII, and gap profiles

Scenario comparison with drill-down to affected instruments and cash flows

Robust IRRBB data quality and monitoring controls

Combine rule-based controls and statistical analysis to identify data quality issues and abnormal movements. Visual indicators and alerts enable teams to investigate anomalies and validate data before it is used for ALCO discussions, supervisory reviews, or internal decision-making.

Automated completeness, consistency, and business checks

Detection of outliers in EVE, NII, and repricing profiles

Workflows for investigation, adjustment, & sign-off

Visual alerts for changes in IRRBB metrics and internal limits

Explore more Opensee solutions

Financial Resource Management

Monitor, stress test, and explain how liquidity, interest rate risk, and capital constraints interact across the banking book.

Liquidity Risk

Monitor, stress test, and explain intraday and structural liquidity across entities and desks—covering cash flow management, regulatory metrics and internal liquidity metrics.

Market Risk

Monitor, explore, and explain real-time VaR, sensitivities, and stress scenarios. Be ready for FRTB SA and IMA, with zero trade-offs between regulatory accuracy and 1LOD/2LOD explainability.

Collateral & Margin Management

Monitor SIMM exposure, optimize collateral allocation, and automate margin workflows in real time, with AI-driven insights and full regulatory audit trails.