P&L and performance attribution with precision

Centralize your data to explain every P&L shift with precision. Link performance, risk, and peer analytics across any portfolio or strategy to get transparent, historical insights for flawless investor reporting and smarter decision-making.

Get a demo

Why asset managers and hedge funds chooses Opensee for P&L & performance

Key capabilities of Opensee for P&L and performance

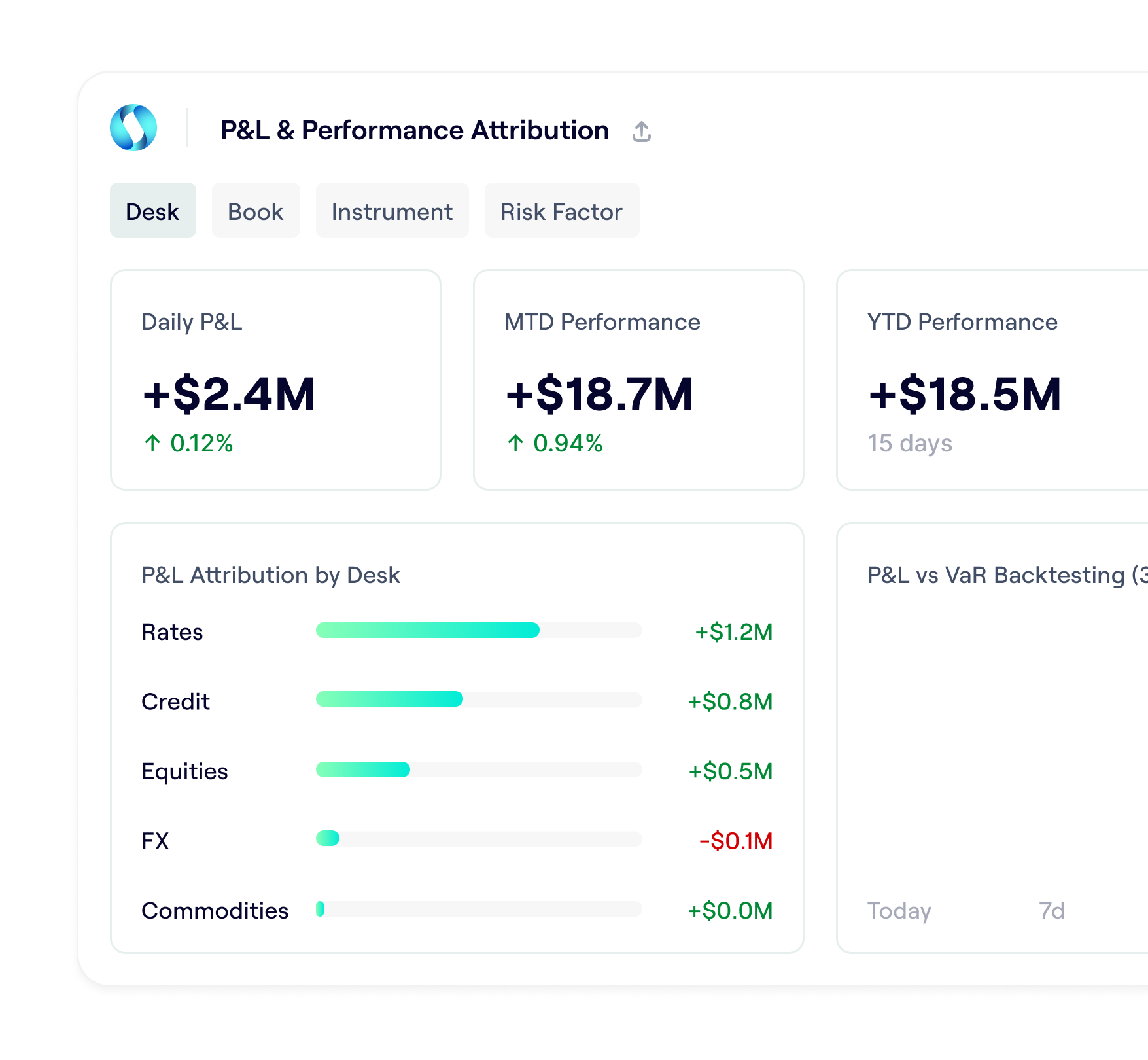

Single repository for P&L, factor exposures, and portfolio positions

Centralize detailed P&L vectors, factor exposures, position data, and NAV components from PM systems, risk platforms, and pricing engines. Data is stored with full versioning and audit trails, allowing to reconstruct historical performance and aggregate consistently across funds, strategies, and asset classes for investor reporting.

Ingest P&L, factor exposures, and positions from OMS/PMS and risk systems

Versioned, auditable data store with full performance history

Multi-dimensional aggregation (fund, strategy, PM, sector, asset class, factor)

Full historical retention for long-horizon performance analysis and backtesting

Instant performance attribution by fund, strategy, sector, or factor

Interactively attribute P&L and performance across any dimension with instant recalculation. Get straightforward aggregations and complex factor-based attribution tied to market moves, enabling seamless transition from fund-level returns to individual position contributions for investor transparency.

Attribute P&L by fund, strategy, PM, sector, geography, or asset class

Drill-down from fund performance to individual position contributions

Factor-based attribution

Benchmark comparison and peer analysis with transparent attribution logic

Connect P&L with risk metrics and factor models

Link P&L vectors with VaR, factor risk models, and risk metrics over unlimited history, enabling systematic performance vs. risk analysis and risk-adjusted return optimization. Compare risk forecasts to realized performance, investigate outliers, and understand where models over- or under-estimated portfolio risk for better investment decisions.

Link P&L vectors to VaR, factor exposures, and risk metrics at position and fund level

Performance vs. risk analysis across multiple years of history

Risk-adjusted return metrics (Sharpe, Sortino, Information Ratio) with drill-down

Support for both regulatory and internal performance/risk diagnostics

AI-assisted performance driver analysis and anomaly detection

Agensee provides AI-assisted driver analysis that highlights key contributors to P&L and performance changes, suggesting relevant drill-downs for PMs and analysts. Built-in anomaly detection spots unusual patterns in P&L vectors, factor exposures, or NAV components—reducing noise, improving data quality, and accelerating explanations.

AI suggestions for funds, strategies, or factors to investigate

Smart drill-down paths to explain large performance movements or deviations

Anomaly detection in P&L vectors, factor exposures, and pricing feeds

Fully auditable adjustments and certifications

Explore more Opensee solutions

Market Risk

Monitor, explore, and explain real-time VaR, sensitivities, and stress scenarios. Centralize risk inputs from multiple sources with zero trade-offs between portfolio transparency, investment agility, and reporting.

ESG Risk

Unify financial and extra-financial data, combine ESG, physical, and transition climate indicators across portfolios and funds, run forward-looking analyses, and support CSRD/ESRS, SFDR, and EU Taxonomy disclosures.

Market Data Store

Get your EOD and intraday market data into Opensee faster and leverage it for analytics and backtesting —saving time on development, maintenance, and support.

Collateral & Margin Management

Monitor SIMM exposure, optimize collateral allocation, and automate margin workflows in real time, with AI-driven insights and full regulatory audit trails.