Collateral & margin management at every level of detail

Monitor SIMM exposure and optimize collateral allocation - from counterparty overview down to individual trade sensitivity, with AI-driven insights and full audit trails.

Get a demo

Why financial institutions choose Opensee for collateral and margin management

Key capabilities of Opensee for collateral and margin management

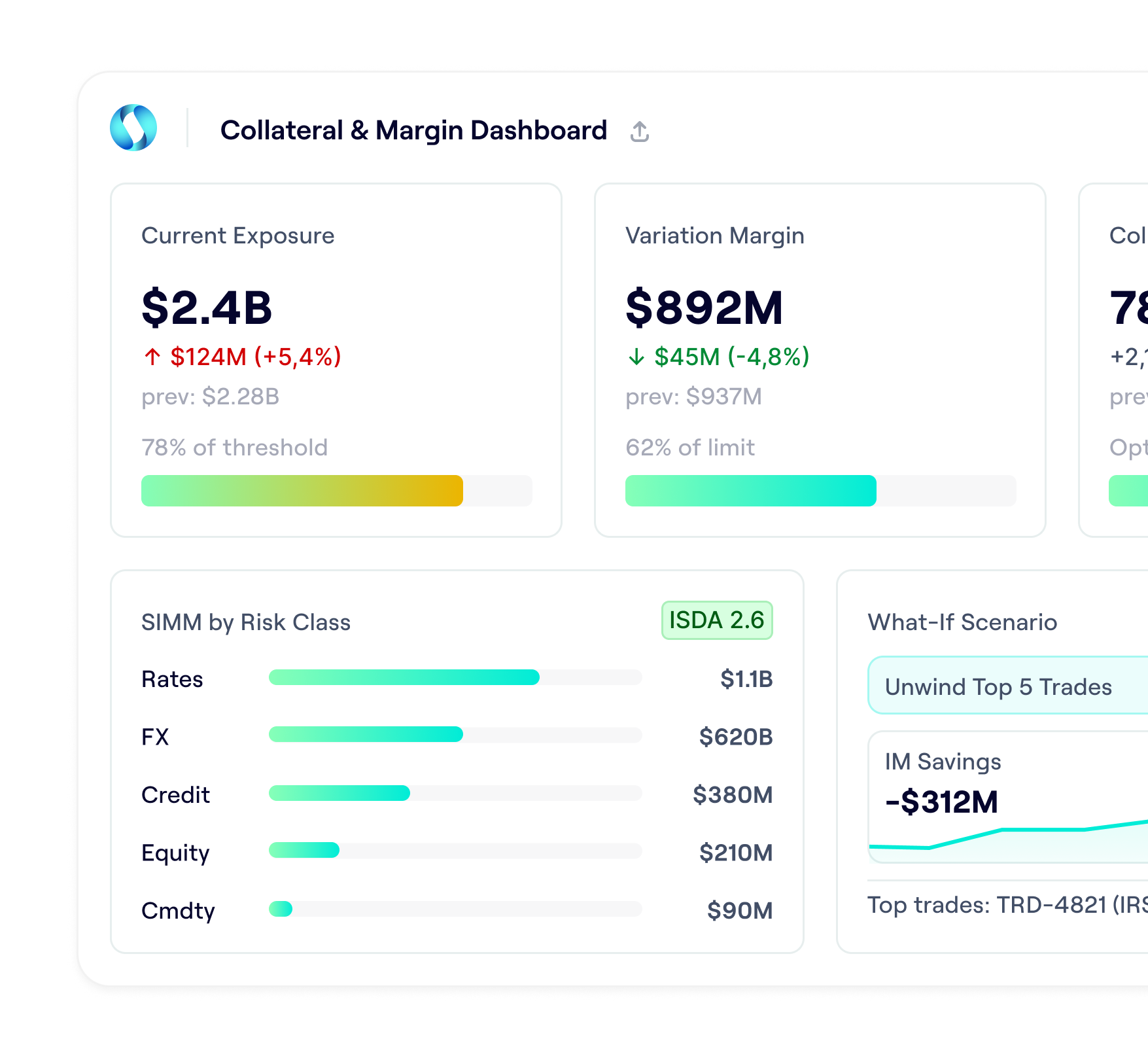

Granular SIMM breakdown from counterparty to trade

Consolidate IM exposure across SIMM, CCP models, and internal add-ons with instant drill-down capabilities. Navigate from total IM to counterparty, netting set, risk class, product class, currency, desk allocation, and individual trade. Analyze sensitivities by bucket, risk factor, tenor, and currency to understand exactly what's driving your margin requirements.

Consolidated view of IM across all counterparties, CCPs, and bilateral agreements

Instant drill-down from portfolio to risk class, product, desk, and trade level

Historical IM trending with day-on-day explain

Support for SIMM, CCP margin models, and custom internal methodologies

Margin impact analysis before execution

Run instant what-if scenarios to quantify the marginal IM impact of new trades, unwinds, portfolio reallocations, or counterparty re-papering. Opensee's simulation engine works on live or versioned datasets, recalculating SIMM exposure in seconds across billions of sensitivities. Support strategic decisions on trade structuring, counterparty selection, and CSA optimization with concrete, data-driven margin projections.

Pre-trade IM estimation at trade, strategy, and portfolio level

Unwind and reallocation simulations to optimize collateral usage

Scenario analysis on market shocks

Backtest alternative collateral strategies and CSA terms before commitment

Optimize collateral allocation across entities and counterparties

Combine collateral inventory, eligibility schedules, haircuts, and concentration limits with real-time margin requirements to monitor the efficiency of your collateral allocation. Analyze funding costs by currency, asset class, entity, and desk. Replay historical collateral allocation decisions and simulate alternative strategies.

Real-time collateral inventory with eligibility, haircuts, and concentration tracking

Funding cost calculations across entities, CCPs, and bilateral relationships

Historical replay and simulation of collateral allocation strategies

AI-driven margin explain and data certification

Agensee identifies key drivers of IM changes and suggests drill-down paths to investigate further. Built-in data quality checks validate completeness, accuracy, and consistency of trade data, sensitivities, and margin inputs. Business users can configure quality rules, certify data, and maintain full audit trails for regulatory compliance.

AI-powered driver analysis for day-on-day IM changes

Anomaly detection in sensitivities, trade attributes, and margin feeds

Configurable data quality checks with certification workflows

Full data lineage and versioning for BCBS 239 and regulatory audit readiness

Explore more Opensee solutions

Market Data Store

Get your EOD and intraday market data into Opensee faster and leverage it for analytics and backtesting —saving time on development, maintenance, and support.

Trade Analytics

Centralize the trading lifecycle into one unified repository, enabling real-time post-trade analysis, MiFID II best execution compliance, and AI-driven pre-trade intelligence to optimize every trade before execution.

Market Risk

Monitor, explore, and explain real-time VaR, sensitivities, and stress scenarios. Centralize risk inputs from multiple sources with zero trade-offs between portfolio transparency, investment agility, and reporting.

Financial Resource Management

Monitor, stress test, and explain how liquidity, interest rate risk, and capital constraints interact across the banking book.