Credit risk analytics for the banking book

Monitor credit risk across retail, SME, and corporate portfolios by exploiting PD, LGD, and EAD outputs, analyzing provisions and RWA, and identifying emerging risks early - with full drill-down from portfolio indicators to individual exposures.

Get a demo

Why banks choose Opensee for credit risk analytics

Key capabilities of Opensee for banking credit risk analytics

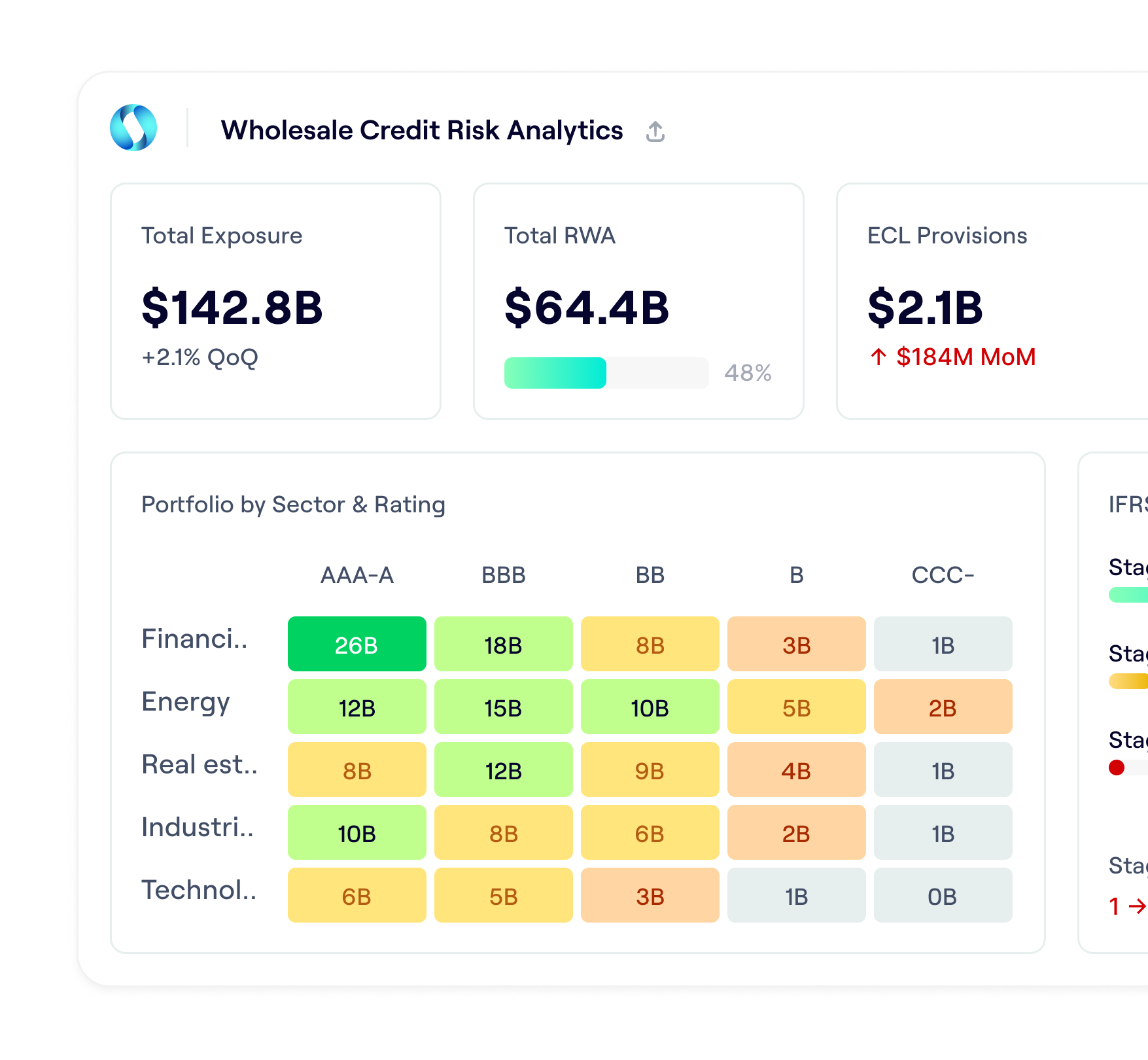

One credit risk view across the entire banking book

Opensee centralizes credit exposures, ratings, PD/LGD/EAD outputs, provisions, and capital metrics across retail, SME, and corporate portfolios. Teams can aggregate and drill down by portfolio, product, geography, or counterparty, with full historical depth and auditability.

Centralized exposure, rating, provision, and RWA data

Coverage of retail, SME, and corporate banking books

Flexible aggregation by portfolio, product, sector, or geography

Full drill-down to facility and counterparty level

Transparent analysis of ECL and RWA movements

Use outputs from IFRS 9 / CECL and regulatory capital engines to provide clear, explainable analysis of ECL and RWA. Users can review staging distributions, track portfolio trends, and understand period-on-period movements with consistent data and traceable calculations.

Analysis of Stage 1 / 2 / 3 exposures and migrations

Consumption and breakdown of 12-month and lifetime ECL results

RWA aggregation and movement analysis

Full lineage from reported figures to underlying exposures

Test portfolio sensitivity to credit and economic shocks

Apply macroeconomic stresses, rating migration overlays, or portfolio-specific shocks to existing credit risk outputs and instantly assess their impact on provisions, capital, and key risk indicators. Opensee supports both internal what-if analysis and supervisory-style stress scenarios.

Application of macroeconomic and credit stress scenarios

Rating migration and PD/LGD sensitivity analysis

Portfolio, sector, and geographic stress views

Immediate impact visibility on ECL and RWA

Identify emerging risks before they materialize

Support regular credit portfolio reviews and early warning monitoring with intuitive analytics. Track exposure growth, rating deterioration, concentration build-up, and provision trends to identify segments requiring attention and support timely management actions.

Portfolio review dashboards for retail, SME, and corporate books

Concentration and exposure trend monitoring

Rating migration and deterioration tracking

Early warning indicators based on portfolio dynamics

Explore more Opensee solutions

Market Risk

Monitor, explore, and explain real-time VaR, sensitivities, and stress scenarios. Be ready for FRTB SA and IMA, with zero trade-offs between regulatory accuracy and 1LOD/2LOD explainability.

Counterparty Credit Risk

SA-CCR, IMM-CCR, SA-CVA, and xVA calculations with full explainability—at any granularity, with sub-second response times on billions of exposures.

Liquidity Risk

Monitor, stress test, and explain intraday and structural liquidity across entities and desks—covering cash flow management, regulatory metrics and internal liquidity metrics.

Collateral & Margin Management

Monitor SIMM exposure, optimize collateral allocation, and automate margin workflows in real time, with AI-driven insights and full regulatory audit trails.