Counterparty credit risk analytics and reporting

Execute SA-CCR, IMM-CCR, SA-CVA, and xVA calculations with speed and precision. Get self-service analytics and AI, run real-time computations and what-if simulations, and ensure superior capital optimization and faster decision-making.

Get a demo

Why banks choose Opensee for counterparty credit risk analytics

Key capabilities of Opensee for counterparty credit risk analytics

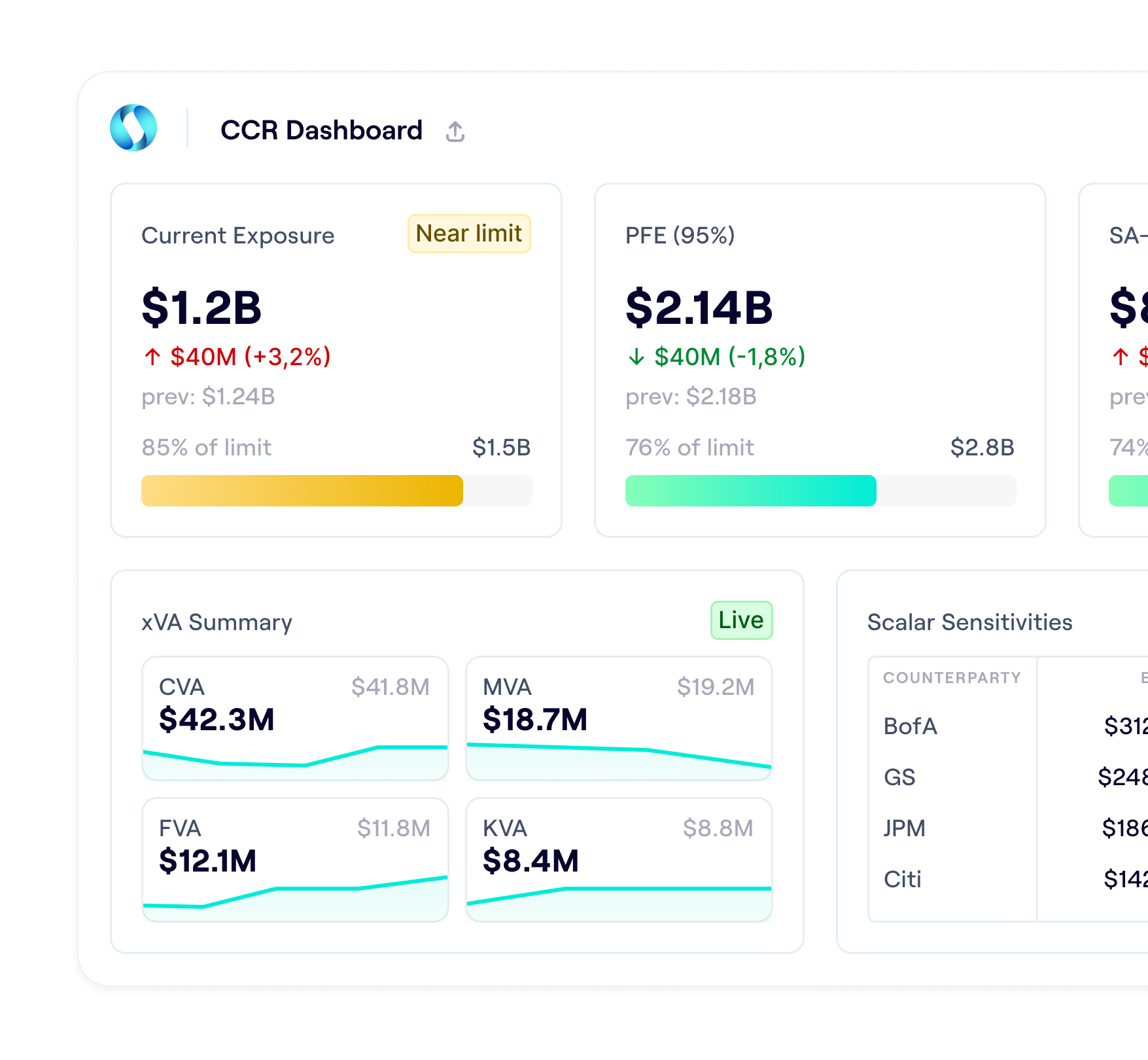

Real-time CCR calculations (EAD, PFE, EPE) and reporting

Compute current exposure, PFE, and EAD in real time under SA-CCR and internal models. Model netting sets, collateral agreements, and off-balance-sheet exposures across all major product types. Aggregate & slice exposures at any level: trade, netting set, counterparty, group, or portfolio.

SA-CCR and IMM-CCR calculations with automated exposure metrics

Support for derivatives, SFTs, and contingent exposures

Real-time netting set modeling and collateral integration

Instant drill-down from portfolio to single trade

SA-CVA, Monte Carlo CVA, and complete xVA on a single platform

Opensee supports both standardized and internal model CVA (including SA-CVA and Monte Carlo-based CVA), integrating market, counterparty, and trade data. Calculate MVA (margin), FVA (funding), and KVA (capital), enabling consistent valuation adjustments and capital analytics across the trading book.

SA-CVA and Monte Carlo CVA with up to 10,000 scenarios

MVA, FVA, and KVA calculations

Real-time drill-down from portfolio-level xVA to trade level

Scenario comparison for xVA sensitivities and hedging strategies

Integrated collateral modeling and credit limit monitoring

Opensee models CSAs and collateral agreements, integrating collateral data directly into exposure and capital calculations. Simulate margin calls, analyze the impact of different collateral strategies on capital, and monitor credit limits at counterparty, group, and portfolio levels with automated breach alerts.

CSA and collateral agreement modeling (eligibility, haircuts, thresholds)

Real-time margin call simulation and collateral impact analytics

Credit limit monitoring with automated breach alerts

Collateral optimization scenarios (cost vs. capital impact)

Agentic AI for CCR explainability and data quality

Agensee works on top of CCR data to help risk teams discover insights faster - suggesting queries, explaining shifts in exposures and CVA, and automating root-cause analysis when capital or limits move unexpectedly. Embedded AI/ML models flag anomalies in CCR feeds (market, trade, or counterparty) before they affect regulatory numbers.

Natural language queries on CCR data

Smart drill-down on exposure and capital changes

AI-driven anomaly detection in CCR and collateral data

Versioned, auditable explanations for internal and regulatory reviews

Explore more Opensee solutions

Market Risk

Monitor, explore, and explain real-time VaR, sensitivities, and stress scenarios. Be ready for FRTB SA and IMA, with zero trade-offs between regulatory accuracy and 1LOD/2LOD explainability.

Banking Credit Risk

Monitor credit risk across retail, SME, and corporate portfolios by exploiting PD, LGD, and EAD outputs, analyzing provisions and RWA, and identifying emerging risks early.

Liquidity Risk

Monitor, stress test, and explain intraday and structural liquidity across entities and desks—covering cash flow management, regulatory metrics and internal liquidity metrics.

Collateral & Margin Management

Monitor SIMM exposure, optimize collateral allocation, and automate margin workflows in real time, with AI-driven insights and full regulatory audit trails.